Nav Guide For Smarter Business Credit Planning

Small business funding often becomes stressful before the owner even applies. A lender may ask for credit history, cash flow, business age, revenue, personal credit, documents, and repayment details, while the owner is still trying to understand what their business profile looks like.

Nav is built to make that picture easier to see. The platform helps small business owners monitor business and personal credit, understand financial health, track cash flow, and explore credit cards, loans, lines of credit, and other financing-related options.

The useful part is not just seeing a score. It is learning what lenders may review, what needs attention, and how to prepare before a business needs capital.

This guide explains how Nav can support business credit planning, what owners should check before looking for funding, and how to use credit and cash flow tools more responsibly.

Why Business Credit Planning Matters

Many small business owners think about credit only when they need money. By then, it may be harder to fix errors, build payment history, or understand why certain funding options are not available.

Business credit planning works better when it happens before the urgent moment. It helps owners see where they stand and what to improve over time.

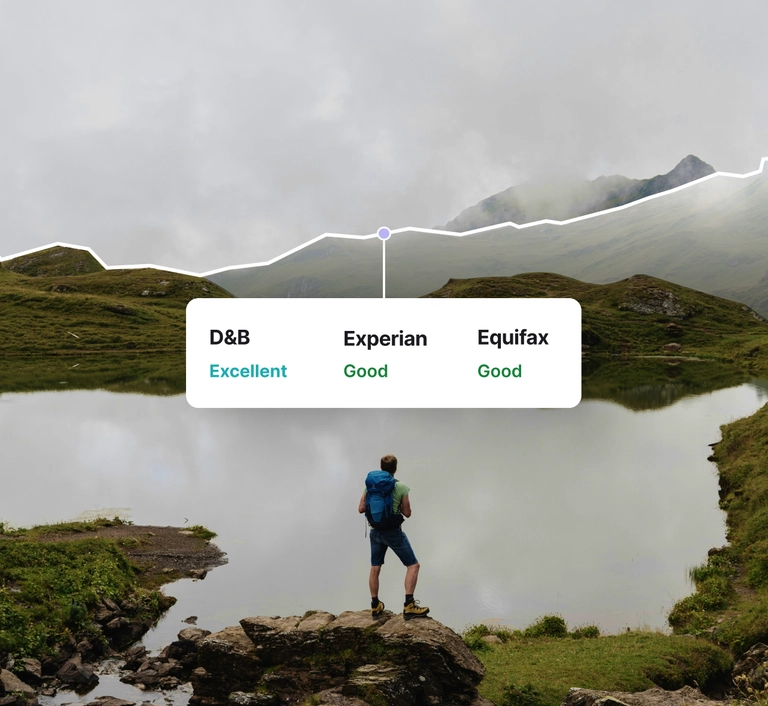

Business and personal credit can both matter

Depending on the lender and product, a small business funding application may involve business credit, personal credit, revenue, cash flow, time in business, industry, and other underwriting factors.

Nav’s homepage highlights the ability to track business and personal credit side by side, which can help owners understand both parts of the picture.

Credit history takes time to build

Business credit is not built overnight. It may involve vendor relationships, payment history, tradelines, business identity consistency, and ongoing monitoring.

Owners who start earlier have more time to identify gaps and create better habits before applying for financing.

Funding readiness is more than a score

A score can be useful, but it is not the entire funding decision. Cash flow, revenue, debt obligations, industry risk, documentation, and business stability can all affect the outcome.

This is why business credit planning should include financial health and cash flow, not only reports.

What Nav Helps Small Business Owners Do

Nav describes itself as a credit and financial health platform built for small business owners. Its official site highlights tools for monitoring credit score progress, accessing credit for a business, tracking cash flow, and using essential business tools.

For owners, the main benefit is having a centralized place to review financial signals that are often scattered across different systems.

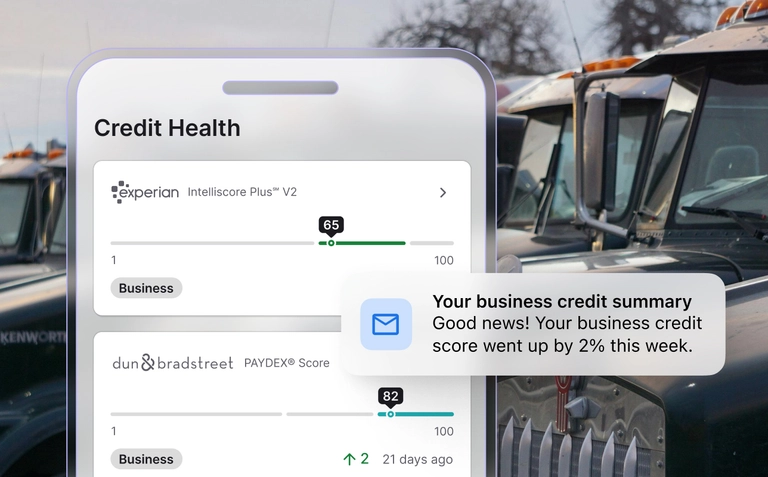

Monitor business credit

Nav Prime plans include credit scores, alerts, and reports from major business credit bureaus such as Dun & Bradstreet, Experian, and Equifax, along with TransUnion-related information.

This can help owners monitor changes, spot potential issues, and understand how their business credit profile may look to outside parties.

Explore funding options

Nav helps users review credit cards, loans, lines of credit, and other financing options through its marketplace and partner network. The platform notes that applications and approvals are still subject to lender underwriting.

This is important because Nav can help with discovery, but it does not guarantee approval or specific loan terms.

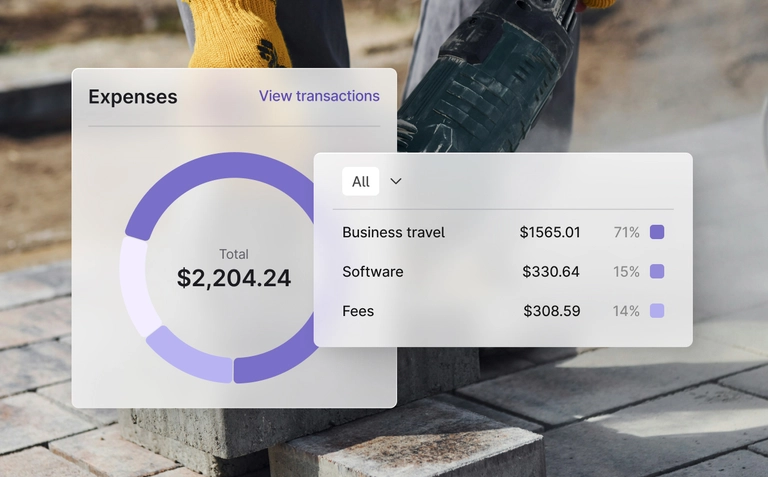

Track cash flow

Nav includes cash flow and bookkeeping-related tools in certain plans. This can help owners understand money movement, spot stress points, and prepare more clearly for tax, financing, or operating decisions.

Cash flow visibility is especially useful for businesses with seasonal revenue, delayed invoices, inventory needs, or growth expenses.

How to Use Nav Before Applying for Funding

The best time to use Nav is before a funding application becomes urgent. That gives the owner time to understand their profile, organize documents, and compare options more thoughtfully.

Use the platform as part of a preparation workflow rather than a last-minute shortcut.

Review your credit profile first

Start by checking your business and personal credit information. Look for missing details, unexpected changes, outdated information, or patterns that may affect lender confidence.

If something looks wrong, investigate it early. Fixing or clarifying credit issues can take time.

Understand your cash flow position

Before borrowing, review whether the business can comfortably handle repayments. Look at recurring revenue, seasonal dips, monthly expenses, tax obligations, payroll, and existing debt.

A funding product should support the business, not create avoidable pressure.

Compare funding by use case

Different funding products fit different needs. A short-term working capital need is not the same as buying equipment, smoothing seasonal cash flow, or covering inventory before a busy period.

Matching funding type to use case can help owners avoid choosing based only on the first available option.

| Business need | What to review | Why it matters |

|---|---|---|

| Working capital | Cash flow timing and repayment ability | Helps avoid repayment strain |

| Equipment purchase | Cost, useful life, and revenue impact | Matches financing to a durable asset |

| Inventory growth | Sales cycle and margin | Checks whether stock can repay itself |

| Credit building | Tradelines and payment history | Supports longer-term profile improvement |

What to Know About Nav Prime

Nav offers membership tiers such as Track, Build, and Expand. The official site lists features including credit scores, alerts, reports, tradeline-related tools on eligible plans, bookkeeping tools, and business credit coaching on higher-tier plans.

Owners should compare the plan features against their current stage before subscribing.

Track is for monitoring

A monitoring-focused plan may make sense for businesses that mainly want visibility into credit reports and alerts. This can be useful for owners who want to watch changes but are not ready for deeper coaching or building tools.

It is also a practical starting point for owners who are just learning how business credit works.

Build is for owners working on credit history

Nav’s Build tier is positioned for growing businesses looking to build business credit with tradeline support. This may appeal to owners who want a more active business credit-building workflow.

Credit-building results vary, so owners should treat this as a process rather than a guaranteed outcome.

Expand is for more guided growth

The Expand tier is positioned for businesses seeking one-on-one guidance and more advanced support. It may fit owners preparing for larger funding goals or trying to understand more complex credit signals.

Before choosing a higher plan, make sure the guidance and tools will be used regularly.

A Practical Nav Workflow for Small Businesses

Nav works best when owners use it consistently. A one-time credit check can be useful, but repeated monitoring gives a clearer view of changes over time.

Use a simple monthly workflow.

- Review business and personal credit changes.

- Check alerts or report updates.

- Review cash flow trends and upcoming expenses.

- Update business information if anything has changed.

- Compare potential funding options only when there is a clear use case.

- Save notes on what improved, declined, or needs follow-up.

- Plan one action for the next month, such as organizing documents or improving payment timing.

Keep business records organized

Funding applications often require business details, revenue information, banking data, tax records, ownership documents, and identity verification.

Keeping these records organized can make the process smoother when an opportunity or need appears.

Do not borrow without a plan

Financing should have a clear purpose. Before applying, know how much you need, how the funds will be used, how repayment will work, and what return or stability the business expects from the capital.

This is a business planning step, not just a credit step.

What Business Owners Should Check First

Before using any financial platform, owners should understand the terms, limitations, and responsibilities involved. Nav is a financial technology company, not a bank, and loan or credit offers are subject to partner underwriting and approval.

Use this checklist before relying on any product or funding option.

- Do you understand which credit reports and scores are included?

- Do you know whether a plan includes tradeline-related features?

- Have you reviewed pricing and billing terms?

- Are you clear that credit-building results may vary?

- Do you understand that funding is subject to lender approval?

- Have you reviewed repayment costs before accepting financing?

- Does the product match a real business need?

Read disclaimers and terms

Financial products can involve eligibility rules, lender underwriting, fees, repayment responsibilities, and reporting limitations. Always review the current terms before subscribing or applying.

For important financing decisions, consider speaking with a qualified financial or tax professional.

Who Should Consider Nav

Nav can be useful for small business owners who want more visibility into business credit and financial health. It is especially relevant for owners who plan to apply for financing later and want to prepare earlier.

The platform may fit several business situations.

- New business owners learning how business credit works.

- Growing businesses preparing for future financing.

- Owners who want to monitor business and personal credit in one place.

- Businesses working on payment history and tradeline visibility.

- Owners who want to understand cash flow before borrowing.

- Businesses comparing funding options with more context.

Ready to understand your business credit and financial health more clearly?

Final Thoughts

Nav can help small business owners understand credit and financial health before funding needs become urgent. Its tools focus on credit monitoring, business credit building, cash flow visibility, financing discovery, and guidance for owners who want to make more informed decisions.

The safest approach is to use Nav as a preparation tool, not a guarantee. Review your reports, understand your cash flow, compare options carefully, and read all terms before applying for financing.

Use Nav to plan business credit and funding readiness more clearly if you want better visibility into credit reports, cash flow, and financing options for your small business.

FAQ

What is Nav used for?

Nav helps small business owners monitor business credit, view financial health tools, track cash flow, and explore funding-related options.

Does Nav guarantee business funding?

No. Funding offers are subject to lender underwriting, approval, eligibility, and terms. Nav can help with discovery and preparation.

Can Nav help build business credit?

Some Nav Prime plans include business credit-building features such as tradeline-related tools, but credit-building results vary by business.

Should I use Nav before applying for financing?

Yes, it can help you review credit, cash flow, and funding readiness before applying. Always check terms and repayment responsibilities before accepting financing.

We only recommend tools we've tested and trust. This post may include affiliate links, meaning we may earn a commission if you choose to purchase - at no extra cost to you.